The $2,500 Wire Transfer: Why Nepal's Restrictive Payment Laws Are Strangling the Digital Dream

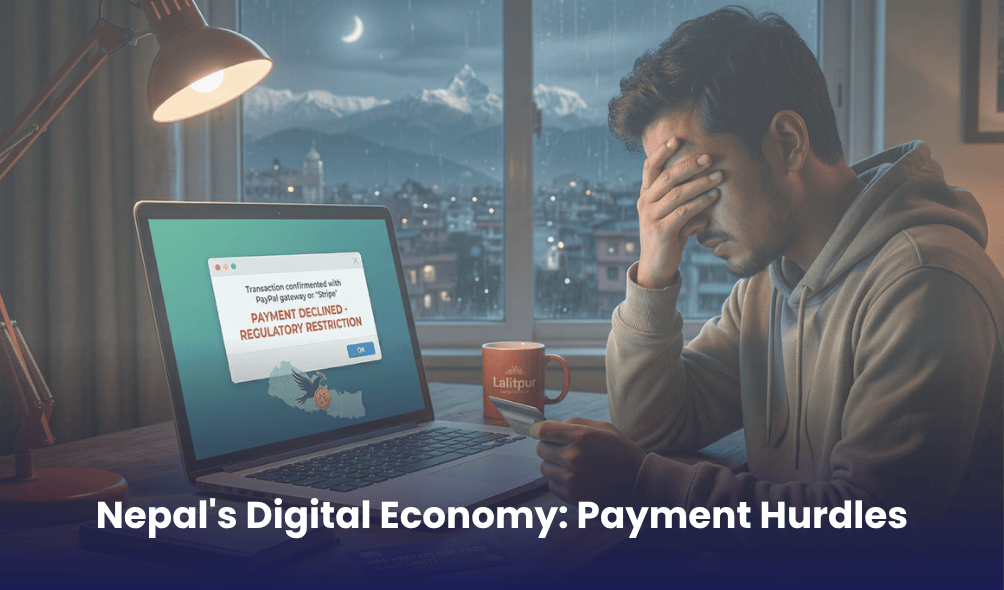

At 3 AM in Lalitpur, Ankit, a 24-year-old full-stack developer, hits "send" on the final code for a Berlin-based marketing agency. His $2,500 monthly invoice is ready. He's technically world-class, but financially, he's a ghost. When his employer attempts a direct SWIFT bank transfer, nearly $100 is swallowed by intermediary fees, and his local bank places the funds on a grueling seven-day "hold" for document verification.

When that fails, Ankit resorts to the "relative loophole." The money is sent to his cousin's PayPal in Australia. Now, Ankit's hard-earned foreign currency is sitting 6,000 miles away. To get it back, he must wait for his cousin to find someone in Australia who needs to send money to Nepal, a classic "Hundi" transaction. Ankit is a success story, yet his native country makes him feel like a financial criminal simply for receiving his salary.

Ankit's struggle is the daily reality for thousands of Nepal's young, skilled freelancers and entrepreneurs. While the world transacts at the speed of light, Nepal remains insulated by a regulatory fortress built on 1960s rules, blocking global payment giants like PayPal and Stripe from full operation. Even worse: while competitors in India, Vietnam, and Bangladesh can click "Pay" and move on, Nepali entrepreneurs must navigate a shadow economy just to survive.

The Great Forex Fear: Structural Vulnerability or Overregulation?

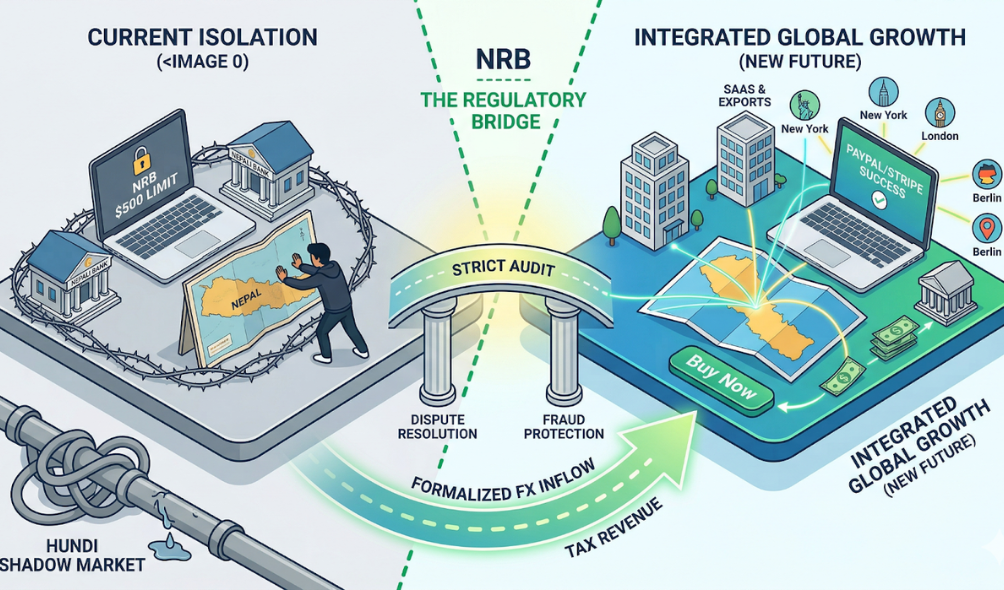

At the heart of the blockade lies the Nepal Rastra Bank, the country's central bank. The regulator's primary concern isn't a lack of technology or expertise; it is macroeconomic survival. Operating under the Foreign Exchange Regulation Act, which dates back to 1963, the NRB tightly manages the flow of US Dollars in an economy chronically dependent on remittances.

As of 2026, this fear contains a kernel of truth. A small, import-dependent economy like Nepal runs on remittances, which account for roughly thirty percent of GDP. The NRB's concern is real but partially overstated: if gateways like PayPal were a true "open valve," allowing citizens to freely spend USD without earning it, the central bank fears a "capital flight" scenario where imports surge faster than remittance inflows can replenish the forex reserves. The mathematics are straightforward—millions of users spending USD reserves faster than foreign earnings refill the pot could theoretically be dangerous.

Yet critics argue this "Strict Gate" approach has created a "Hundi Paradox." By blocking formal channels, the NRB unintentionally forces the entire digital export sector into the illegal shadow market. This means the precious USD generated by Nepali freelancers and tech companies—potentially hundreds of millions annually—never enters the national reserve. It stays in offshore accounts, Hundi networks, and informal channels, invisible to the state and untaxed. The irony is sharp: the regulation meant to protect foreign reserves may actually be depleting them.

The Shadow Market and the Vendor Workaround

Because direct payment is restricted, a massive shadow market has emerged. If you want Netflix, YouTube Premium, or Spotify in Nepal, you likely don't pay the company directly. Instead, you pay a "reseller" on Facebook or Instagram via eSewa, marking up the price by fifteen to thirty percent. These resellers often use international cards obtained through relatives abroad or purchased on high-fee grey-market channels. It is an inefficient, unregulated, and risky shadow economy that benefits no one except the middlemen.

Even in the business sector, the friction is substantial. While local vendors have emerged to provide AWS server hosting, Google Workspace, and Microsoft Azure licenses, their margins are considerable. For a lean startup, having to go through a vendor instead of clicking "Pay" on a dashboard adds bureaucratic drag that competitors in India or Vietnam simply don't face. A SaaS company in Kathmandu might pay twenty percent more for the same cloud infrastructure simply because of NRB rules.

The Tourism Friction Tax

Nepal is a world-class destination operating on antiquated payment rails. For a tourist in London booking a trekking expedition, a SWIFT wire transfer is a five-day ordeal. Modern travelers demand instant "Buy Now" buttons and digital wallets. The lack of direct integration is a "friction tax" that favors large international booking aggregators like Viator or GetYourGuide over local agencies.

A trekking guide in Pokhara or a pottery teacher in Bhaktapur cannot easily collect deposits or process refunds, leaving them vulnerable to no-shows and reducing trust. Seeing the PayPal or Stripe logo at checkout provides immediate psychological trust; without it, local businesses look unprofessional to the global traveler. This isn't hyperbole foreign tourists choosing international platforms over local operators represents a real loss of revenue to Nepal's tourism ecosystem.

The $500 Sandbox: A Baby Step with Potential

In 2021, the NRB issued a critical directive: the Prepaid USD Card. This was a controlled experiment designed to allow individuals to load up to five hundred dollars per year onto a card, then spend it globally on international websites and services. It formalized thousands of previously informal transactions.

The cap sounds like a straightjacket. Five hundred dollars per year isn't enough for any growing tech company, AWS, Figma, and Slack together exceed five hundred dollars per month. Yet what many don't understand is that the NRB built flexibility into the system. If a cardholder can prove they generate foreign income double the card amount, the central bank allows additional deposits beyond the base five hundred. So a freelancer earning five thousand dollars from Upwork might qualify for a two thousand dollar card. However, this "flexible tier" is opaque, and banks apply it inconsistently.

There's another layer of nuance: the NRB permits individuals to deposit up to five thousand dollars annually from international sources. The spending limit of five hundred dollars per year is separate from this earning limit. This distinction is crucial because it shows the NRB has already admitted that some bi-directional flow is safe.

The Revenue Problem: Taxing the Invisible

Here lies a compelling paradox that policymakers often overlook: the government has established a five percent final tax for digital exports, but it only works if the money hits a Nepali bank. A Stripe integration would create a transparent paper trail. For the tax office, five percent of a formalized digital economy is infinitely better than zero percent of a hidden one.

Ankit is technically supposed to report his twenty-five hundred dollar monthly income and pay five percent tax. But because he cannot receive money directly through formal channels, his real income is invisible. He pays zero dollars in tax to Nepal. If Stripe were allowed to operate with proper Know-Your-Customer checks, Ankit would formally be taxed, and the government would collect approximately fifteen hundred dollars annually from him alone. Multiply that by fifty thousand freelancers earning USD abroad, and the country is leaving seventy-five million dollars or more on the table every year.

This blind spot represents a fundamental misalignment of the NRB's objectives. Openness doesn't mean losing control; it means gaining visibility. A formalized digital export sector would generate substantial tax revenue and allow for better macroeconomic planning. Instead, the current regime simply pushes activity into shadow channels where neither the state nor legitimate businesses benefit.

The Actual Risk: What the NRB Gets Right and Wrong

The NRB's concerns warrant serious consideration, but they are often overstated. The central bank is right to worry about unrestricted payment flows, a sudden spike in import-heavy spending could indeed strain forex reserves, and weak KYC procedures could create money-laundering vulnerabilities. These are legitimate risks that any prudent regulator should monitor.

Where the NRB's logic breaks down is in the comparisons that justify its restrictions. Policymakers often point to Nigeria's 2023-2024 currency crisis or Sri Lanka's 2022 collapse as cautionary tales about what happens when capital flows are liberalized. But these analogies don't hold up. Nigeria's naira plunged because oil prices crashed and the government removed fuel subsidies overnight, policies that sent inflation soaring to nearly thirty percent. Sri Lanka's rupee collapsed after tourism revenues dried up from the 2019 Easter bombings and COVID-19 devastated the sector, compounded by massive external debt service. Neither crisis had anything to do with PayPal or digital payment gateways. The NRB conflates different economic problems: what happened in Lagos or Colombo reveals nothing about what would happen if eSewa and Khalti could process international payments. The central bank is using the wrong case studies to justify the right concerns.

The Path Forward

Nepal's digital potential is trapped in a regulatory sandbox while the rest of the world moves forward. India, Bangladesh, and Vietnam have already allowed PayPal and Stripe to operate with proper oversight. Their economies didn't collapse.

Meanwhile, Nepal is losing its most talented youth to brain drain. Ankit will likely move to Bangalore within two years, not because he doesn't love Nepal, but because his bank account there will function. He's not alone, thousands of young developers and entrepreneurs face the same choice.

The path forward is neither reckless nor revolutionary. The NRB should issue clear guidance on expanded prepaid card tiers, allow local financial companies to operate as regulated gateways, and engage with PayPal and Stripe on data residency requirements. The one-way valve has served its purpose. It's time to turn it into a two-way street.

The two-thousand-five-hundred-dollar wire transfer that cost Ankit one hundred dollars and ten days of waiting, that's not the sound of a country protecting itself. That's the sound of a country falling behind.